Revolutionizing Industries: The Power of Blockchain Technology in the United States

Revolutionizing industries across the United States, blockchain technology is reshaping the way businesses operate, ensuring transparency, security, and efficiency. As a decentralized digital ledger system, blockchain has the potential to disrupt traditional models in sectors such as finance, healthcare, supply chain management, and more. Its ability to create immutable records of transactions has made it a cornerstone for innovation in the digital age. From reducing fraud to streamlining processes, blockchain is proving to be a game-changer for American enterprises.

The Evolution of Blockchain Technology

Blockchain technology was first introduced in 2008 with the creation of Bitcoin by an anonymous individual or group known as Satoshi Nakamoto. Initially seen as a tool for cryptocurrency, its underlying technology quickly gained attention for its broader applications. The core concept of blockchain lies in its distributed ledger system, where data is stored across a network of computers rather than a single central server. This decentralization makes it resistant to hacking and tampering, offering a level of security that traditional systems often lack.

As the technology evolved, so did its use cases. In the United States, companies and government agencies began exploring blockchain for purposes beyond cryptocurrency. The rise of smart contracts—self-executing agreements with the terms directly written into code—further expanded blockchain's utility. These contracts automatically enforce and execute agreements when predefined conditions are met, reducing the need for intermediaries and increasing efficiency.

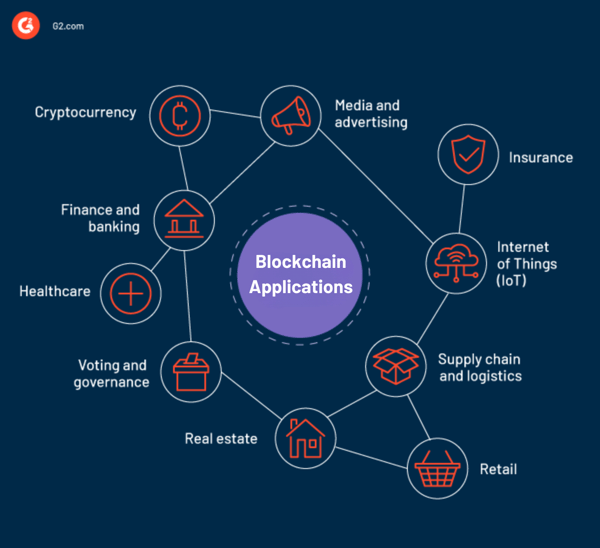

Applications in Key Industries

One of the most prominent areas where blockchain is making an impact is in the financial sector. Banks and financial institutions are leveraging blockchain to streamline cross-border payments, reduce transaction costs, and enhance security. Traditional banking systems often involve multiple intermediaries, leading to delays and higher fees. With blockchain, transactions can be processed in real-time, significantly improving the speed and cost-effectiveness of financial services.

In the healthcare industry, blockchain is being used to secure patient data and improve interoperability between medical providers. Electronic health records (EHRs) stored on a blockchain can be accessed by authorized parties while maintaining privacy and integrity. This not only enhances data security but also ensures that patients have control over their own health information. Additionally, blockchain is being explored for tracking pharmaceuticals, helping to combat the issue of counterfeit drugs and ensuring that medications reach consumers safely.

Supply chain management is another sector experiencing a transformation through blockchain. By providing a transparent and tamper-proof record of product movements, blockchain enables companies to track goods from production to delivery. This increased visibility helps prevent fraud, reduces errors, and improves overall efficiency. For instance, major retailers are using blockchain to trace the origin of products, ensuring ethical sourcing and sustainability.

Government and Regulatory Landscape

The adoption of blockchain in the United States is not without challenges. While the technology offers numerous benefits, it also raises concerns regarding regulation, scalability, and energy consumption. The U.S. government has been cautious in its approach, balancing innovation with the need for oversight. Various federal and state agencies are working to establish frameworks that support blockchain development while protecting consumers.

At the federal level, the Department of Commerce and the National Institute of Standards and Technology (NIST) are actively involved in researching and developing standards for blockchain technology. Meanwhile, states like Arizona and Nevada have taken proactive steps by recognizing blockchain-based records and digital signatures in legal contexts. These initiatives demonstrate a growing acceptance of blockchain as a legitimate and valuable tool for modern governance.

Challenges and Future Prospects

Despite its promise, blockchain technology still faces several challenges. Scalability remains a significant issue, as many blockchain networks struggle to handle a large number of transactions efficiently. Energy consumption is another concern, particularly with proof-of-work blockchains like Bitcoin, which require substantial computational power. However, innovations such as proof-of-stake consensus mechanisms are being developed to address these issues.

Looking ahead, the future of blockchain in the United States appears promising. As more industries recognize its potential, investment in blockchain startups and research is expected to grow. Additionally, the integration of blockchain with emerging technologies like artificial intelligence and the Internet of Things (IoT) could unlock new possibilities. From enabling decentralized finance (DeFi) to enhancing cybersecurity, blockchain is set to play a pivotal role in shaping the digital economy.

Conclusion

Blockchain technology is revolutionizing industries across the United States, offering a secure, transparent, and efficient alternative to traditional systems. Its applications span various sectors, from finance and healthcare to supply chain management and government operations. While challenges remain, ongoing advancements and regulatory support are paving the way for broader adoption. As the technology continues to evolve, it is clear that blockchain will remain a driving force in the digital transformation of American businesses and institutions.

Comments

Post a Comment